[ad_1]

India is mentioned less than five times, and only once in a headline, in Mary Meeker’s 340-page Trends: Artificial Intelligence report. Yet, it has been making waves in the technology community since its release in May. One reason for its popularity is that Meeker, an influential technology analyst since the early days of the internet, has released such a report after a four-year hiatus. Another is that she offers sharp insights on the themes relevant to India—AI adoption, pricing, impact on the labour market, and the country’s position in an ever-shifting AI landscape.

Global spread

The launch of OpenAI’s ChatGPT kick-started the current interest in AI. The speed at which ChatGPT’s users grew was unprecedented. It took ChatGPT just two months to reach 100 million users compared to Instagram’s 2.5 years, WhatsApp’s 3.5 years, and Facebook’s 4.5 years. Equally important is the speed of its international reach. The ChatGPT app reached a point where 90% of its users were outside North America in its third year, a milestone that took the internet 23 years to achieve.

India played a key role—it accounts for 13.5% of global ChatGPT mobile app users as of April 2025, compared to the US’ 8.9%, driven by India’s 886 million internet users, mostly via smartphones. Over 153 million smartphones were shipped in 2024 alone, according to Counterpoint Research. Besides, ChatGPT supports many Indian languages, including the top six. India also accounts for 6.9% of DeepSeek mobile app users, the third largest after China and Russia.

Pricing power

Major AI platforms, including ChatGPT, Google’s Gemini, Anthropic’s Claude, and Perplexity, all offer a free tier for users, which explains India’s share in the mobile apps. The premium versions of these platforms are about $20 per month, and more advanced versions could cost $100 to $250 per month. The pricing is global and doesn’t take into account purchasing power. (Low prices are key to capturing the Indian market. India’s telecom tariffs, for example, are among the world’s lowest.) For AI companies, subscription and developer API fees are key.

However, the report points out that the AI landscape is competitive, with well-funded tech incumbents, emerging challengers, and a growing open-source movement all vying for market share. Besides, the performance gap between closed-source and open-source models is narrowing, putting pressure on pricing power. Whether this would lead to telecom-style lower costs is not clear yet.

Labor market

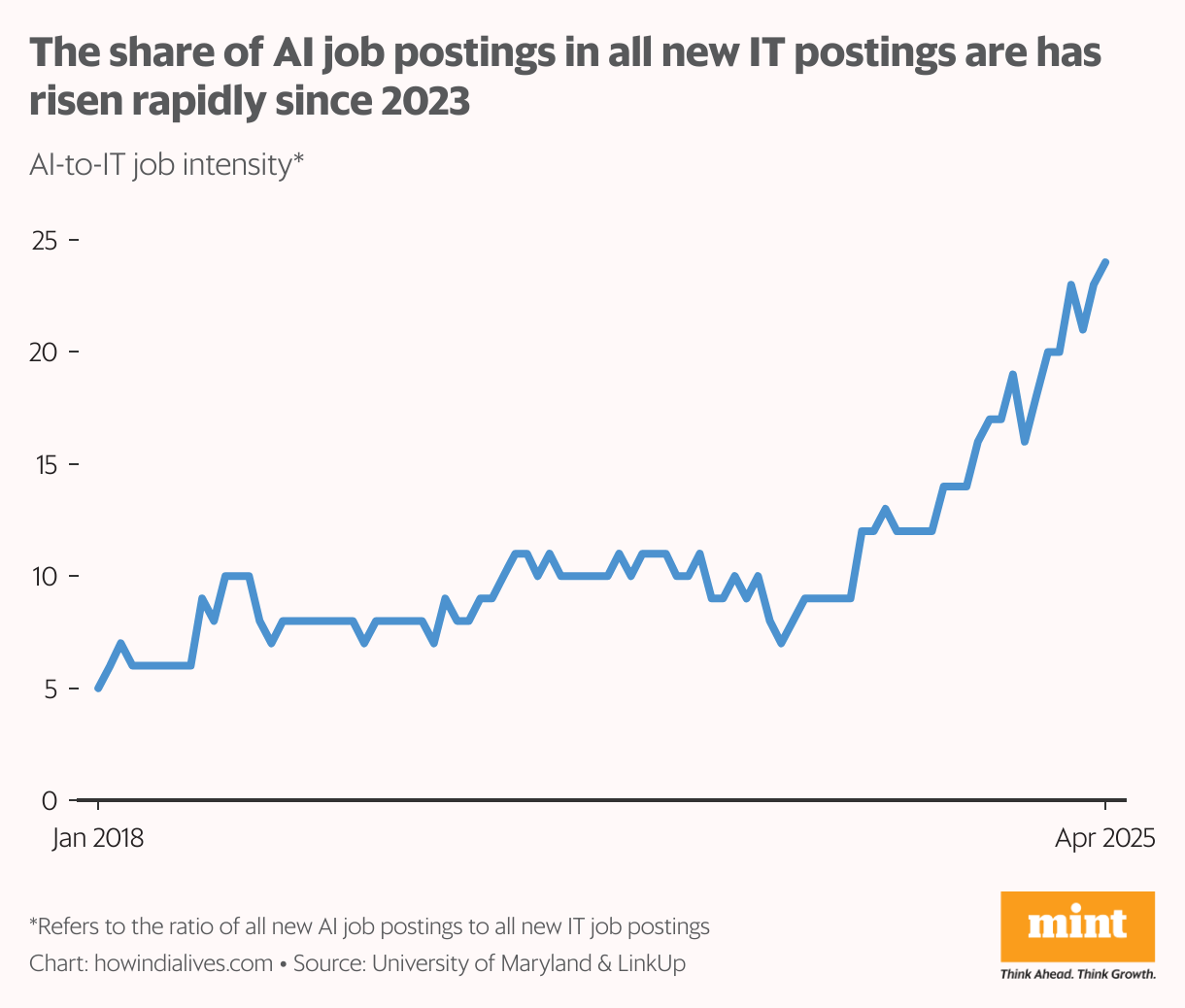

Mary Meeker highlighted a clear shift in demand away from traditional IT roles toward those requiring AI skills. While AI-related IT job postings in the US increased by 448% between January 2018 and April 2025, non-AI IT job postings declined by 9% over the same period. The cumulative number of new global job titles containing AI terms grew by 200% between Q2 2022 and Q2 2024. Beyond creating new titles, companies are integrating AI skills as a core competency for their entire workforce.

Companies like Duolingo and Shopify state that AI use is now a “baseline expectation” and will be factored into hiring and performance reviews. This shift is especially important for Indian IT services companies, which grew by offering US tech skills at a lower cost. The changing job market must be reflected in their workforce too, validating their recent investments in AI training for employees.

AI factories

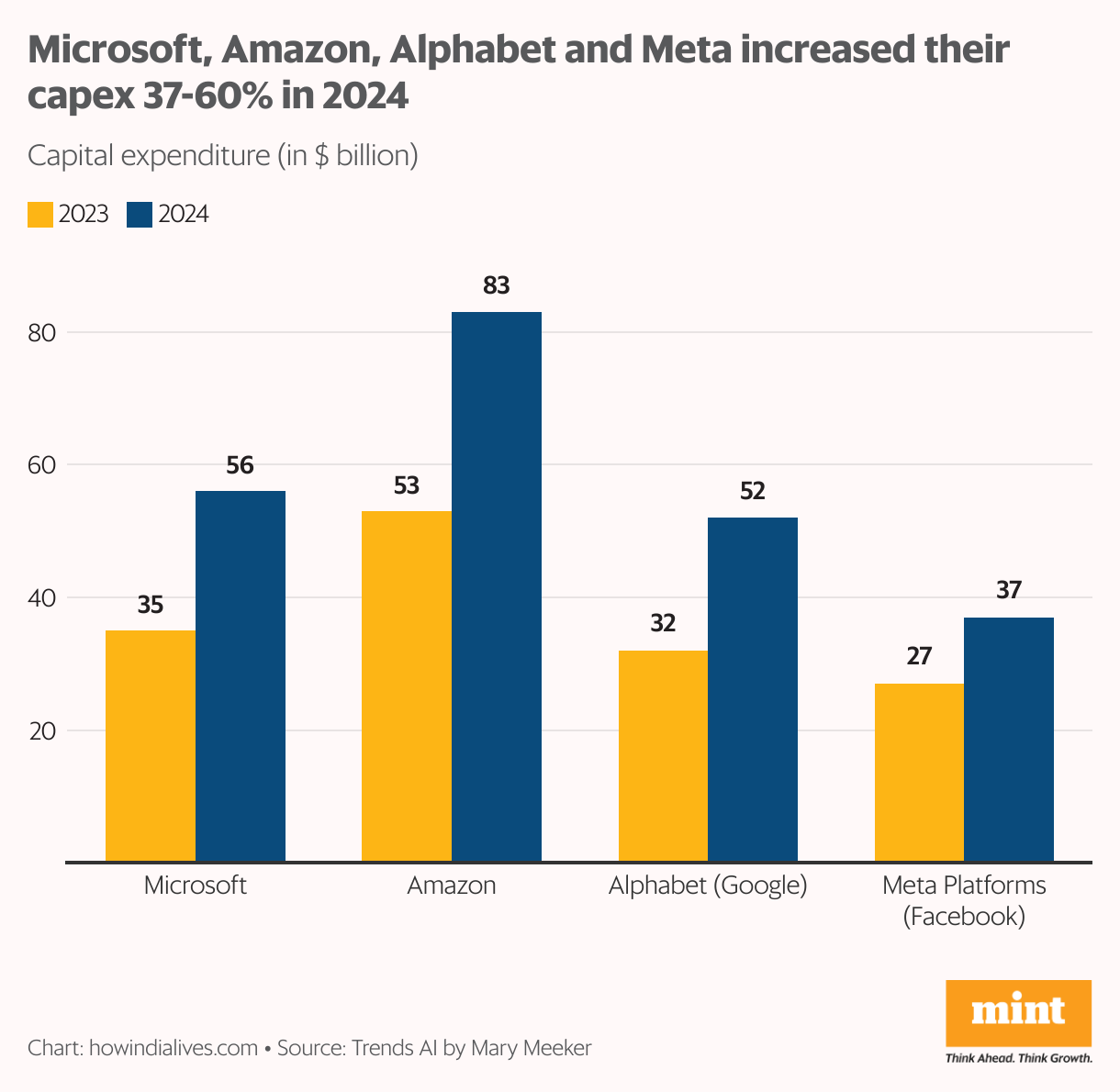

While Indian IT services companies are “right-skilling” their employees, the big tech companies in the US are investing in “AI factories”, as the report describes the data centres. Microsoft, Alphabet, Amazon, and Meta spent $228 billion on CapEx in 2024, a 55% increase year-over-year. CapEx of the Big Six (including Apple and Nvidia) has grown at a 21% annual rate over the last decade and now represents 15% of their total revenue, up from 8% a decade ago.

A significant portion has gone into building hyperscale data centres, faster network infrastructure, and acquiring specialised hardware like GPUs and custom AI accelerators. They’ve also increased R&D spending to 13% of revenues in 2024, up from 9% a decade ago. This spending is fueled by immense financial strength—these companies collectively generated $389 billion in free cash flow in 2024 and held over $443 billion in cash. They are using these resources to invest aggressively in what they see as the next fundamental wave of technology. Indian companies lack this financial capacity, partly explaining the AI pessimism in India.

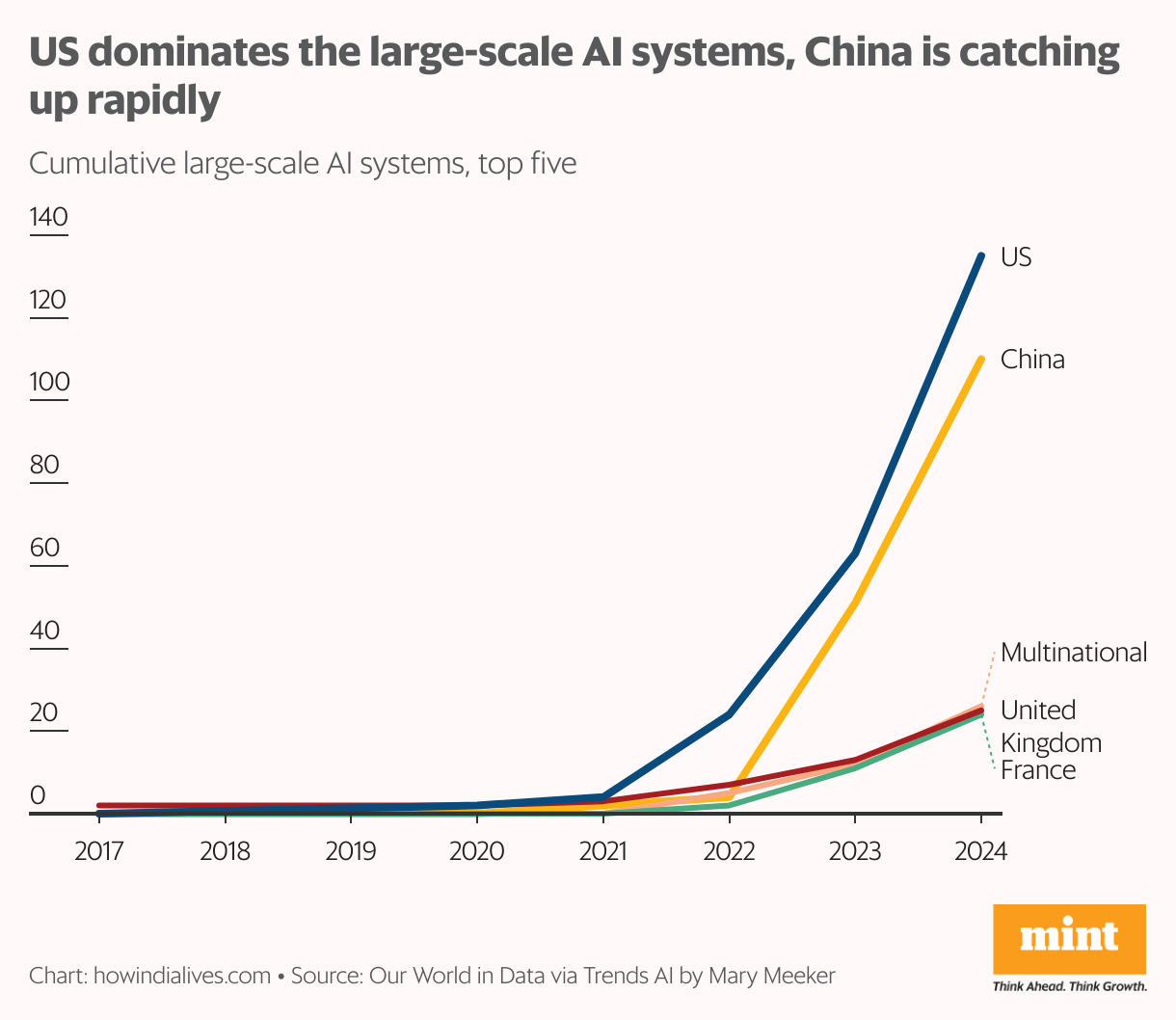

The two-power race

These investments have positioned the US as the leader in AI systems, followed by China, with both far outpacing the rest of the world. China has dramatically accelerated its AI capabilities through national initiatives like “Made in China 2025″. Chinese AI models from DeepSeek, Alibaba (Qwen), and Baidu (Ernie) are rapidly closing the performance gap with US counterparts, often at lower training costs. AI now underpins China’s nationally strategic areas, including battlefield logistics and cyber operations, raising US concerns.

The report quotes Microsoft’s Brad Smith, noting that China recognises that if a country standardizes on its AI platform, it will likely rely on that platform in the future. The US response, therefore, should be “not to complain about the competition but to ensure we win the race ahead”. Other countries are taking notice. More nations, including India, are increasingly pursuing “Sovereign AI” policies to build domestic computing capacity using their own infrastructure and data.

www.howindialives.com is a database and search engine for public data.

[ad_2]

Source link

{kind=link}